Economics : 2012 : CBSE : [Delhi] : Set II

To Access the full content, Please Purchase

-

Q1

Give meaning of an Economy.

Marks:1View AnswerAnswer:

An economy is the business of one place to another. Economy can be defined as "Activities related to the production and distribution of goods and services in a particular geographic region.”

-

Q2

What is Market Demand?

Marks:1View AnswerAnswer:

Market Demand is simply the horizontal summation of all the individuals’ demand of the consumers in an economy.

-

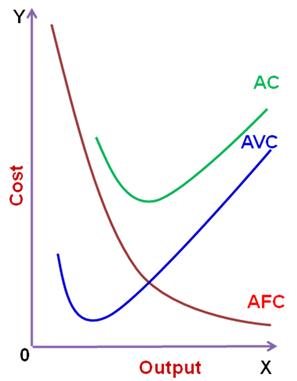

Q3

What is the behavior of average fixed cost as output increases?

Marks:1View AnswerAnswer:

As output increases, average fixed cost falls.

-

Q4

What is the behavior of average revenue in a market in which a firm can sell more only by lowering its price?

Marks:1View AnswerAnswer:

Average Revenue curve slopes downwards in a market in which firm can sell more only by lowering the price.

-

Q5

What is price taker firm?

Marks:1View AnswerAnswer:

Price taker firm is a firm which has no control over the existing market price and cannot influence it. A firm in a perfect competitive market is regarded as a price taker firm.

-

Q6

A producer borrows money and opens a shop. The shop premise is owned by him. Identify the implicit and explicit cost from this information. Explain.

Marks:3View AnswerAnswer:

The implicit cost will consist of

a.Imputed rent of the shop

b.Imputed value of his own services

The explicit cost includes the interest to be paid on the money borrowed.

Implicit cost (borrowed cost) refers to the cost of the factor that a fixer neither hires or purchase. It is not actually paid by the producers but includes in the cost of production. It is a difference between the economic profit and the accounting profit. On the other hand, explicit costs are those costs which are borne directly by the firm and paid to the factors of production. -

Q7

What is ‘Marginal Rate of Transformation’? Explain with the help of an example.

Marks:3View AnswerAnswer:

Marginal Rate of transformation gives the amount of Y that must be sacrificed in order to gain an additional unit of X with full and efficient utilization of available resources. It is also known as opportunity cost.

-

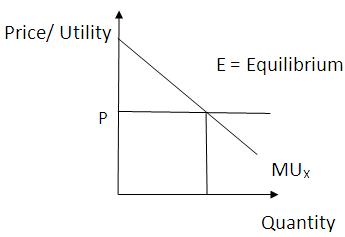

Q8

Given price of a good, how does a consumer decide as to how much of that good to buy?

Marks:3View AnswerAnswer:

If a consumer has to decide on which good to buy at a given price, the consumer should compare Marginal utility (MU) of that good with its price (P). The consumer will be at equilibrium when the Marginal utility of the good will be equal to the price of the good.

i.e. MUx = Px

If MUx > Px , which means price is less than Marginal utility derived from that good, them the consumer will buy more of that particular good.

-

Q9

Draw Average Variable Cost, Average Total Cost and Marginal Cost Curves in a single diagram.

Marks:3View AnswerAnswer:

-

Q10

Explain the implication of large number of buyers in a perfectly competitive market.

Marks:3View AnswerAnswer:

There are large number of buyers and sellers in a perfectly competitive market. The numbers of sellers is so large that no individual firm has any control over the price of the commodity. Due to large number of sellers in the market, there exists a perfect and free competition. A firm acts as a price taker while the price is determined by the’ invisible hands of the market’. That is, interaction of demand and supply determines the price of the commodity. Therefore, in a perfectly competitive market, a firm is a price taker and not a price maker.