Economics : 2011 : CBSE : [Delhi] : Set III

To Access the full content, Please Purchase

-

Q1

What is a market?

Marks:1View AnswerAnswer:

In economics, a market refers to whole of the region in which buyers and sellers of a commodity are in close contact to effect sale and purchase of the commodity. Essential ingredients of the market are:

(1) Commodities and services are bought and sold.

(2) Area having communication between buyers and sellers.

(3) Close contact between buyers and sellers. -

Q2

When is a firm called ‘price-taker’?

Marks:1View AnswerAnswer:

Under perfect competition, price of a commodity is determined by the interaction of market demand and market supply of the whole industry. No individual firm can influence the price because its share in the total supply is insignificant. Every firm has to accept the given price and adjust the output. The firm can sell at this price as many units of the commodity as it wants. It is because of this reason the firm is said to be price taker.

-

Q3

Define budget set?

Marks:1View AnswerAnswer:

The budget set is the set of bundles of goods that an agent can afford. This set is a function of the prices of goods and the agent’s endowment.

-

Q4

What is meant by ‘increase’ in supply?

Marks:1View AnswerAnswer:

Shift in supply curve is defined as change in supply due to factors other than the price of the good. If supply curve shifts rightward, it shows increase in supply.

-

Q5

Define supply.

Marks:1View AnswerAnswer:

Supply refers to the quantity of a commodity that a seller is willing to sell at a given price in a given period of time.

-

Q6

Why is production possibility curve concave? Explain.

Marks:3View AnswerAnswer:

Production possibilities curve is based on the assumption of increasing marginal rate of transformation (MRT). Due to this, PPC is always concave to the origin. The slope of PPC represents the marginal rate of transformation between two commodities, i.e., the rate or ratio at which one commodity is sacrificed in order to increase the production of another commodity by one unit. Increasing MRT states that the rate of sacrifice of one good in order to increase the production of another good increases with production of every additional unit of the latter commodity. Due to this, the production possibility curve is always concave to the origin.

-

Q7

8 units of a good are demanded at a price of Rs 7 per unit. Price elasticity of demand is (-)1. How many units will be demanded if the price rises to Rs 8 per unit? Use expenditure approach of price elasticity of demand to answer this question?

Marks:3View AnswerAnswer:

As elasticity is = 1, change in demand is equal to change in price as shown below:

As total expenditure remains the same, it shows elasticity of demand is = 1. Here at price Rs 8, number of units demanded will be 7.Price per unit (Rs) Quantity Demanded (Units) Total Expenditure (Rs) 7 8 56 8 7 56 -

Q8

Giving examples, explain the meaning of cost in economics.

Marks:3View AnswerAnswer:

Cost of producing a good is the sum of actual expenditure on inputs and imputed expenditure on inputs supplied by the firm itself.

For example: A firm requires factor inputs (land, labour, capital) and non-factor inputs (fuel, power, raw-material) for producing a commodity. These inputs are to be paid since they are scarce in supply. The firm pays in the form of money like – wages, rent, interest etc. These costs to the firms are termed as money cost.

In economics, the sum total of explicit and implicit cost constitutes the total cost of production.

Explicit Costs: These are the cash payments that firms make to outsiders for their services and goods.

Implicit Costs: These are costs of self-owned, self-supplied resources. -

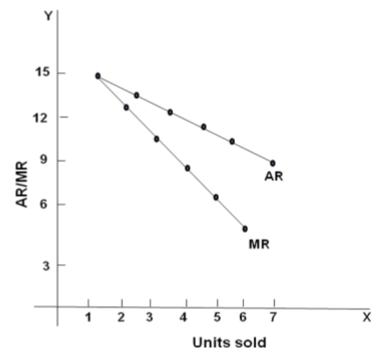

Q9

Draw average revenue and marginal revenue curves in a single diagram of a firm which can sell more units of a good only by lowering the price of that good. Explain.

Marks:3View AnswerAnswer:

Monopoly: It refers to a market situation where there is a single firm selling the commodity and there is no close substitute of the commodity.

Monopolistic Competition: It refers to a market situation in which there are many firms that sell closely related but differentiated products.

In a monopoly market and monopolistic market (i.e., non-competitive markets), more units of a product can be sold only by reducing the price. This means AR declines with sale of every additional unit. Therefore, MR is less than AR (MR< AR). The AR and MR curves of the firm become downward sloping. In the figure, MR curve does not coincide with AR curve but remains below it. The reason for it is the different nature of AR and MR. MR is limited to one unit whereas AR is derived by all the units resulting in comparatively lesser fall in MR.

-

Q10

For blind candidates in lieu of Q No 9.

Distinguish between Average Revenue and Marginal Revenue with the help of a numerical example.Marks:3View AnswerAnswer:

Average Revenue: AR is the revenue per unit of the product sold.

Marginal Revenue: Marginal revenue is the addition to the total revenue from sale of an additional unit of a commodity.

Relationship between AR and MR:

o AR increases as long as MR is higher than AR.

o AR is maximum and constant when MR is equal to AR.

o AR falls when MR is less than AR.

o MR can be negative but AR can never be negative.In a perfect competition, where any amount of a commodity can be sold at the same price, MR=AR. The reason for it is, the industry is the price maker and the firm is the price taker. A firm has to accept the price as determined by the industry. The firm can sell any amount of the commodity at this price which means with sale of every additional unit, additional revenue (MR) and average revenue (AR) will be equal to the price and thus, equal to each other (MR= AR = Price). This fact is explained by the below mentioned table.

Units Sold

AR

TR

MR

1

15

15

15

2

15

30

15

3

15

45

15

4

15

60

15