Economics : 2011 : CBSE : [ All India ] : Set II

To Access the full content, Please Purchase

-

Q1

Define production function.

Marks:1View AnswerAnswer:

Production function represents technological relationship between physical input and output of a product. In other words, it shows that with a given state of technology and during a particular period of time, how much we can produce with the given inputs. Symbolically, production function can be written as follows:

Q = f (f1, f2, f3.......f4)

f1, f2, f3 are factors of production.

Four factors of production used in the production process are land, labour, capital and entrepreneur.

-

Q2

When is a firm called price maker?

Marks:1View AnswerAnswer:

A monopoly firm is called price maker because it has full control over the price. Goods produced by the monopolist do not have close substitutes.

-

Q3

Define a budget line.

Marks:1View AnswerAnswer:

The budget line represents all the commodities which a consumer can purchase with his entire money income. Let us have two commodities X and Y. Their respective prices are P1 and P2. The entire income of the consumer is Rs 100. The budget line will be written as follows:

P1x + P2Y = 100 -

Q4

What is ‘decrease’ in supply?

Marks:1View AnswerAnswer:

When the supply of a commodity falls due to change in factors other than price, it is called decrease in supply. Under this, leftward shift of supply curve takes place.

-

Q5

Define money.

Marks:1View AnswerAnswer:

Money can be defined as anything that is generally acceptable as means of exchange and acts as a measure and store of value.

-

Q6

Define an economy?

Marks:1View AnswerAnswer:

Economics is a social science that studies the economic activities of human beings concerned with allocation of resources with optimum efficiency.

-

Q7

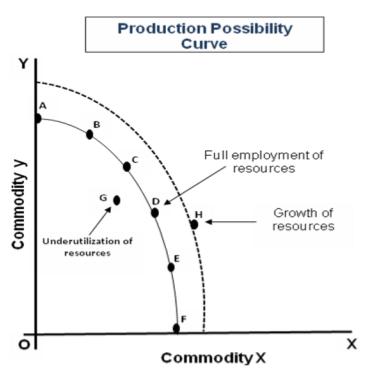

How is production possibility curve affected by unemployment in the economy? Explain.

Marks:3View AnswerAnswer:

A production possibility curve represents the maximum productive capacity in the economy as it is based on fuller and efficient utilisation of resources. PPC will shift towards left only in case of destruction of resources which causes a decrease in productive capacity in the economy.

However, unemployment of resources does not affect the productive capacity in the economy. It represents under utilisation of resources and hence in case of massive unemployment, the actual production combination will lie inside the production possibility curve, i.e., point G.

-

Q8

Distinguish between explicit cost and implicit cost and give examples.

Marks:3View AnswerAnswer:

(i) Explicit costs are those cash payments that firms make to outsiders for their services and goods. It is the money expenditure incurred on purchasing and hiring of inputs. While, implicit cost is the cost of self owned and self employed resources.

(ii) In case of explicit cost, payment is made to others, but in case of implicit cost, payment is not made to others. It becomes due to the owner for use of his own factors of production.

(iii) Examples are:

Explicit cost: Expenses on hiring factor inputs like services of land, labour, capital etc. and non factor inputs like, raw material, power etc.

Implicit cost: An entrepreneur utilises his own building or his own capital or may act as a manager of his firm himself.

-

Q9

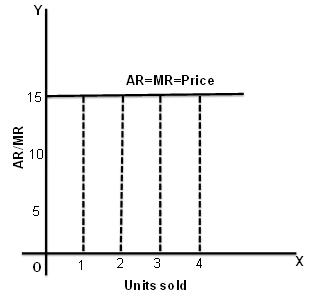

Draw in a single diagram the average revenue and marginal revenue curves of a firm which can sell any quantity of the good at a given price. Explain.

Marks:3View AnswerAnswer:

Average Revenue: It is the revenue per unit of the product sold.

Marginal Revenue: Marginal revenue is the addition to the total revenue from sale of an additional unit of a commodity.

Under perfect competition where any amount of commodity can be sold at a given price, MR=AR. The industry under perfect competition is the price maker and the firm is the price taker. The firm can sell any amount of commodity at this price and with sale of every additional unit. The additional revenue (MR) and average revenue (AR) will be equal to each other.

-

Q10

Note: The following question is for the Blind Candidates only, in lieu of Q. No.9.

Explain the relation between average revenue and marginal revenue of a firm which is free to sell any quantity at a given price.Marks:3View AnswerAnswer:

Marginal Revenue (MR) is the extra revenue that an additional unit of product will bring to a firm. It can also be described as the change in total revenue/change in number of units sold.

MR=

Average Revenue is defined as the revenue per unit of output. It is obtained as:

AR =

Relationship between marginal revenue and average revenue:

- When MR is greater than AR, AR rises.

- When MR is equal to AR, AR is constant.

- When MR is less than AR, AR falls.

The following schedule shows the relationship between MR and AR.

Total Output

Total Revenue

Average Revenue

Marginal Revenue

1

2

3

4

5

6

9

16

21

24

25

24

9

8

7

6

5

4

9

7

5

3

1

-1